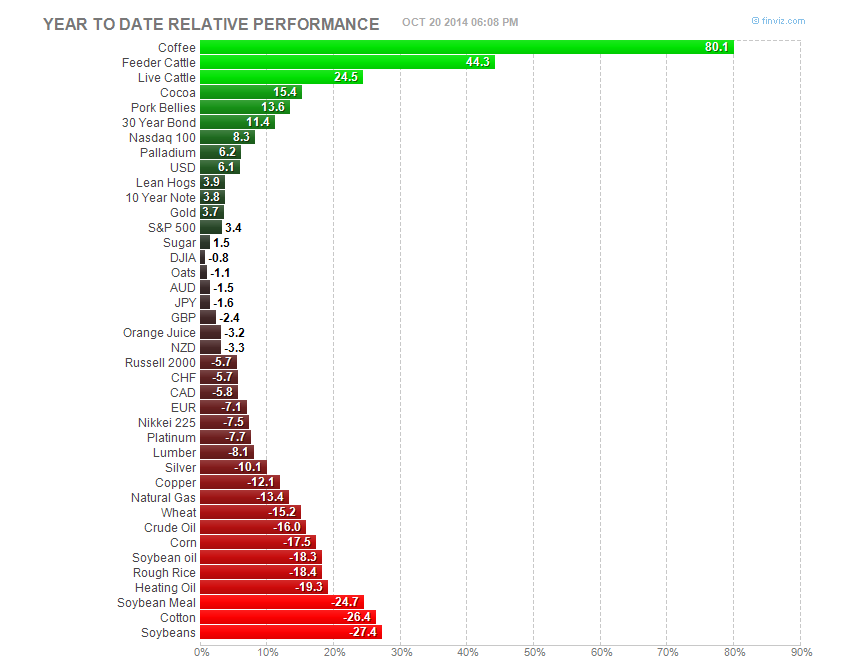

OK, after a long absence, I'm posting this book review just because I feel like it. It's my personal opinion:

Thomas Piketty's bestselling door-stopper Capital in the Twenty First Century notes some facts that he thinks point to a clear problem and solution:- The return on capital over the economic growth rate determines the Capital/Income ratio, where a higher return on capital implies higher level of capital relative to income (r/g --> C/I)

- The rate of return on capital has been pretty consistently around 4.5%,

- The rate of growth grew from 0.9% in the 19th century to 2.4% in the 20th, peaking around 1950

- Growth was 3.8% in Europe in the Les Trente Glorieuses ("The Glorious Thirty") of 1945-75, when marginal taxes and taxes on inheritance were higher, and income became more equally distributed

![]() |

| 'Peek-et-ee' |

To him, the implication is obvious. Raise taxes back to what they were in the good old days of Les Trente Glorieuses to reduce inequality. The point of the tax is not so much to increase revenues but rather to âexpose wealth to democratic scrutiny" (p. 471) and thus "regulate capitalismâ (p.518). As with all really popular nonfiction, it hits the zeitgeist because many think democracy and equality are paramount unalloyed objectives, so a big book scientifically proving these noble objectives are under a vicious assault is highly welcome; nothing rallies the troops like news of an attack. Plus, the new tactic is refreshingly more feasible, as making the rich poorer is a lot easier than making the poor richer.

However, the good times he cherishes are what econometricians would call an overidentified event: there are several different correlates that could statistically 'explain' the 1950s. When I was growing up it was common for progressives to caricature the 1950s as a period of bigotry, materialism, and conformism, now those same progressives consider this a golden age; What if the key to reducing inequality is bigotry? Maybe

econometrics shows we need to decimate, in the original

Roman sense, our young men every other generation to make them hard working and less whiny.

![]() |

| Tax Rates over time |

![]() |

| Capital/Income over time |

Most importantly for his case is the fact that because marginal taxes, and inheritance taxes, were so high, the rich had a much different incentive to hide income and wealth. He shows marginal income and inheritance tax rates that are the exact inverse of the capital/income ratio of figures, which is part of his argument that raising tax rates would be a good thing: it lowers inequality. Those countries that lowered the marginal tax rates the most saw the biggest increases in higher incomes (p. 509). Perhaps instead of thinking capital and top-income proportions went down when taxes were raised, it was just reported less to avoid confiscatory taxes? Alan Reynolds

notes the many changes in the 1980s US tax code that explain the rise in

reported wealth and income irrespective of the actual change in wealth an income in that decade, and one can imagine all those loopholes and inducements two generations ago when the top tax rates were above 90% (it seems people can no better imagine their grandparents sheltering income than having sex, another generational conceit).

For example, he writes that Lilian Bettencourt, the richest woman in France and heiress to the L'Oreal fortune (mentioned often, she serves as the archetype of the rich), never reported more than a $5MM annual income on a $30B fortune, a 0.02% annual return. Given his assumed 5% return on capital, and that given Bettencourt's true returns have been above this average, this implies that it is clearly possible for reported income to stray from actual income by a factor of 100 for a long time. Given this feasibility and the incentives given by changing marginal tax rates and various corporate laws, it seems highly possible the whole U-shaped pattern in capital/income and top-decile-income/total income is just people sheltering their income at various intensities given the tax rate over the past century.

Finally, on the Capital/Income ratio trending upward again towards the 6:1 level of the

Belle Ãpoque (1871-1914), his idea is that structural forces in the returns on inherited capital are driving inequality. Yet, if you take

housing out of his data the recent rise in Capital/Income disappears. Housing is not presumed to be concentrated in the top 1% or 10%, but rather across the top 50%, and further, it seems to have an anomalous trend in his sample (i.e., the housing bubble over the past 30 years), so if housing is the cause of recent capital ratio increases, it's not the driver increasing top incomes, the 'r>g' explanation fades into a distraction. So while I agree inequality is increasing, his diagnosis of the genesis (an abnormally high return on inherited wealth relative to economic growth) seems unlikely, and with a bad diagnosis, his cure is worthless.

![]() |

| The 1% of the Deep |

He calls the consequences of the long-term dynamics of wealth distribution "potentially terrifyingâ (p. 571). At one point he notes "15% of income was transferred from the poorest 90% to the top 10%" (p. 297) as if the rich simply took it from the middle class, and so the success of the rich just implies more theft, more injustice. Further, âimmense inequalities of wealth have little to do with the entrepreneurial spirit and are of no use in promoting growth. Nor are they of any 'common utility,'" meaning, they do not contribute to growth, nor count in his social welfare function, Mussolini's "everything within the state, nothing outside the state." In sum, his main concern is that the rich don't create wealth, they mainly just take it from others, and so social justice is negatively related to their wealth. Stalin's thoughts on the Kulaks were similar.

Piketty argues against a problem that is theoretically not a problem: the rich getting richer holding all other things equal. It is undoubtedly true that the poor today are rich compared to 50 years ago, having access to microwaves, the internet, air-conditioning, etc. that were the either confined to the rich or not available to anyone, yet it seems to many as if today's poor are worse-off than they were in the 1950s, highlighting that as a practical matter poverty is relative. Standard economic models do not capture that. My book

The Missing Risk Premium argues that as a descriptive matter economics is not sufficiently dismal, in that people are more motivated by envy than greed. I never thought one should do this, and think it better for society and your own wealth and happiness to replace envy with greed, and act as most standard economic models assume. That is, most economic models assume people are simple non-envious wealth maximizers, while most people aren't really like that. This is kind of depressing, because if the key to social happiness is merely material equality, there are many ways to do that, most of them terrifying.

Clearly many economists clearly think like Piketty, that we

should be more focused on relative status (i.e., envy) over simple absolute welfare. Thus, economics currently is quite confused because all of their canonical models are based on standard utility functions that ignore relative status, yet they don't really believe it. This is a profound confusion, and the profession should focus attention on it because if you are using assumptions you don't really believe, it's rather pointless. Yet, Piketty merely attacks inequality without any serious discussion of how, exactly, wealthier rich people is worse than poorer rich people. It is petty and perverse to assert that a year where the stock market rises 20% is worse than one where it only rises 5%, because of its effects on inequality. Intellectuals generally hate evangelical Christians in good part because they are so similar in temperament and their preoccupation with

eschatology; progressives are the new Puritans, whose haunting fear is that someone outside the state may be rich and not even feel guilty.

What is the optimal level of inequality? He notes we cannot know for sure, but then immediately argues we should reduce it because it's too high (many times he qualifies remarks in one place, acts as if the qualifications don't exist in another). If inequality within a country is bad

per se, should we curtail unskilled immigration (after all, immigration was much lower in

Les Trente Glorieuse)? Is the inequality of capitalism worse than that of politics? Note Chelsea Clinton is currently paid $75K for a speech, surely not due to any trenchant analysis of today's issues, but rather, she's part of a political dynasty. Jeb Bush's son is often mentioned as a potential Presidential candidate, and so too Hillary Clinton. US Vice President Joe Biden's son is on the board of a Ukrainian gas company, probably not because he is expert at energy logistics. Nepotism is less common in business than politics because shareholders lose patience with the founder's grandson much quicker than voters lose patience with the latest Kennedy, Gandhi, or Papandreou.

One of the great things about a market economy and corporations is that it has created a unique pre-eminence of reciprocal altruism over familiar altruism. Corporate institutions need highly developed contractual relationships among strangers, which breeds trust and a lack of corruption, a better society, while its alternative is nepotism (where markets are not strong, trust is low and clans dominate). Further, corporate competition is positive sum because of productivity growth, unlike state competition which often involves war (what's better, a price war or a war war?). Extreme democratic egalitarianism invariably leads to economic stagnation and

illiberal tyranny, a bug dismissed by Marx, though its continuance over the next century suggests this has been no accident. I would gladly like to have an experiment where one state emphasized democracy and egalitarianism, the other self-reliance and bourgeois morality, if only so I could move to the latter.

![]() |

| Bad People |

Certainly the eras that gave us our scientific and intellectual heritage were very unequal, with not just an aristocracy but often slavery. If some inequality is inevitable, how much is too much or too little? When the West was beginning its industrial revolution and creating an unprecedented growth in productivity and social welfare, giving us the railroad, electricity, indoor plumbing, the internal combustion engine, etc., Piketty notes wages were 'objectively miserable' in the 19th century as if they could have been higher but for elite cupidity, and the

Belle Ãpoque evokes the specter of exploitation. The fact that the

average height was rising and

infant and maternal mortality rates were falling at an unprecedented rate after stagnating for centuries if not a millenium, supposedly means little. So too the great increase in technology that economist

Robert Gordon notes was not only unprecedented, but singular, never to be achieved again. In Piketty's mind it's an unbearable time, reminding me of the scene in Monte Python's

Life of Brian where John Cleese says, apart from the aqueduct, sanitation, peace, roads, etc., "

what have the Romans done for us?"

Piketty does admit that âprivate property and the market economy do not serve

solely [my emphasis]

to ensure the domination of capital over those who have nothing to sell but their laborâ, as demonstrated by the failure of the Soviet Union. This rather weak acknowledgement reminds me of what the esteemed Keynesian economist and communist apologist Joan Robinson said about markets fifty years ago: "the market may not be a good master, it can be a useful servant." Faint praise betrays a deep antipathy.

Liberals consider Piketty's book a must-read, but only because, like Marx's

Capital, it's a great safety blanket for Liberal prejudices. The end-game is exactly what progressive conventional wisdom (e.g., the common New York Times or Harvard professor view) has been preaching for over 50 years: enlarge the state. The key point is a highly credentialed academic wrote a long book proving that some abstruse mathematical inequality (r>g) implies we need to raise taxes on the rich and regulate wealth more democratically. It's really the debating tactic called 'spreading', which is to put forth so many arguments, none sufficient or necessary, that you can always claim victory. For example I could question his many empirical assertions, such as how could German inflation have averaged only 14% from 1913-1950 (p. 545) given inflation was 10^10 in 1923, or his theoretical assertions, such as how

depreciation affects his r/g=C/I steady state equilibrium, but that would leave another 20 assertions unstained, and so those who want to euthanize

renteirs can retain faith in their big picture.

Piketty is a modern progressive, best defined as someone who thinks intellectuals should run everything as the vanguard of the people, which is why academics, journalists, and writers are predominantly progressive. Hayek noted that scribes have always been egalitarian, probably always lamenting the fact that the idiots in power don't write nearly as well as them, and thus, are objectively less qualified but via some tragic flaw in the universe, end up in power. It forms the common

reverse dominance hierarchy so common today, where obsequious, hypocritical yet articulate and confident leaders pander to the masses and rule via democracy, focusing their envious eyes on those who aren't interested in that game, such as those concerned with business, religion, or

their own family. As Piketty notes, "if we are to regain control of capitalism we must bet everything on democracyâ (p. 573), he says from his inegalitarian and very undemocratic position at the Paris School of Economics.

It never occurs to them that the main problem with subjecting markets to democratic control is that those who end up wielding power will be incompetent or tyrannical, and that 'the people' have never ruled directly, only their various proxies. Every totalitarian government of the 20th century has rested on at least the perception of massive popular support, which is why they have all ruled in the name of The People. An unchecked democracy becomes mob rule or ripped apart by factions, why the Founding Fathers, so familiar with Greek history, were careful to put checks and balances in the US constitution and emphasize the republican nature of government.

![]() |

| Good People |

Democracy, like all things, is good only in moderation; it is a means and not an end. Taken to an extreme it is highly dysfunctional, as decisions are not helped by making them mass plebiscites or town hall meetings. Go to a school board meeting and watch how quickly thoughtful discussions get sidetracked. Philip Howard's

Rule of Nobody outlines an interesting consequence to increasing public participation in big decisions. As the number of stakeholders grows each interest group seeks its own group's ends without moderation, they are single-issue advocates nobly advancing their righteous cause (e.g., Native Americans, aquifers, unions), and so veto action unless they are basically paid-off. The result is that usually nothing happens, and so the days when we could build the interstate highway system, the Hoover Dam, or the Empire State Building in only a year, are over. Small 'd' democratic control of property leads to stasis, why government spending today is mainly on transfer payments and studies, not roads and bridges.

Another problem with democracy is that as opposed to decentralizing power to the people it does the opposite. As the Occupy movement showed, unorganized mass movements get nothing done, so successful parties are those that channel public legitimacy into a small set of essential rights too important to be outside state dominion. Go to a school board meeting and watch how insiders anticipate idiotic comments from the rabble, and so control the outcome to make such meetings basically Potemkin village town halls. Eventually the organization-committed people take over the organization and the mission-committed people become frustrated and leave (see a

description of the recently created regulator CFPB's quick descent into solipsism). They set up national plans for health care, education, energy, etc., and slander choice and variety as a 'race to the bottom.' Thus, teachers unions and Medicare/Medicaid focus on preventing choices that might take away from centralized power, competition from other providers and exit by consumers is outlawed.

![]()

Piketty never delves into the various public choice problems that beset collective action. Progressives are still stuck in the syllogism: democracy is good, the world has problems, therefore we need more democracy. The probable result of the democracy-fetishist end-game is not another Soviet Union, but rather, a Venezuela or Argentina. Venezuela's pathetic case is well-known, but few are aware Argentina was as prosperous and free as the US at the beginning of the 20th century. The Argentine state's role in the economy increased more than average in the twentieth century, reflected in the increase in state-owned property, regulation and higher levels of public spending. They emphasized Keynesian macroeconomic policy, aimed at the redistribution of wealth and the increase of spending to finance populist policies. Most importantly for this book, they implemented a wealth tax around 2000. Currently GDP/capita there is about one-fourth of that in the USA, and this is not compensated by some

Bhutanese quality of life metric.

Piketty often quotes Marx, and like Marx he ignores the endogeneity of growth and the return on capital on things like taxes, and simply assumes the growth is basically exogenous. He notes that Africa is poor and has a much lower capital/income ratio than in Europe yet he never explores this, and for a good reason: across countries, the levels and movements in the Capital/Income ratio

do not correlate well with income inequality. To think that greater taxes will bring income inequality back to the 1950s via the

Trente Glorieuse in Europe and the US correlation of tax taxes and growth is just cherry picking a broad panel dataset to support your prejudices.

His central prescription is a world-wide wealth tax and more democratic regulation of wealth, which would require a global wealth monitoring system, a good scenario for the next Tom Cruise blockbuster (

The Piketty Report where Tom and Scarlett Johansen try to move their kid's college fund into bitcoin). He never even considers it a disturbing increase in state control. As Piketty notes, it didn't work at all when Greece tried to raise taxes on its rich in the recent fiscal crisis because the rich could move themselves or their capital abroad, the strategy must be a coordinated, region-wide if not world-wide effort. A strategy that is not coalition-proof is not feasible, and raising punitive taxes on the rich is a good example. Marxists dislike competition, the best regulator and innovating mechanism in human history, so thinking one can avoid it via a global monopoly is consistent with their delusional utopian worldview.

The key to good economics was first shown by Adam Smith: showing the emergent properties of individual behavior. They key is to have good assumptions as to what motivates individuals, and the basic idea of Smith was that people want to make themselves more prosperous, an innocuous assumption with surprising results. Piketty's muse, Marx, on the other hand, was clearly wrong on his assumptions, such as assuming the value of something is directly proportional to the labor it embodies, or supposing that people would float between being artisans, poets, miners, farmers, in the same day. Good assumptions are essential for a useful theory, and Marx didn't have them.

![]() |

| Don't Blame Him |

Georg Wilhelm Friedrich Hegel, Marx's muse, was more insightful on human nature. He thought people want recognition from society for oneâs labors, as vocations are often chosen and mastered as part of a personâs own search for meaning. Being appreciated by others doing something you were not forced to do, something not everyone can do, gives great satisfaction. When you have to work at something that takes only effort you feel unimportant; your agency is not appreciated by others and when you die you'll be soon forgotten. Hegel noted that in agriculture people are mainly busy addressing immediate material needs. Thus, duty was a strong Protestant ethic because working hard to feed your family was necessary and psychologically onerous, so many found comfort in the thought their hard work was part of God's plan. Given the prerequisites needed for the industrial and scientific revolution, perhaps it was.

Only in what Hegel called the âsecond estateâ of trade and commerce can people become independent and have freedom. Homer's Achilles chose to die with eternal honor rather than to live forever in unimportant obscurity, and it resonates because it exaggerates a choice many of us would make, as impacting others positively is in many ways more important than our own life. The defeat of natural necessity is a prerequisite for the development of the free individual and of ethical life for Hegel. Thus, in spite of the higher mortality rates of cities, people have always migrated to urban areas in their own search for meaning, the chance of life more than mere subsistence was enough to motivate many. People want higher status via their own individual essence. Having children, for example, is probably the most common way people do this, and it should be noted that if people today were simply maximizing their wealth they wouldn't have kids; they clearly want to connect to the future, not just consume.

![]() |

| Mickey Kaus |

The beauty of this instinct is that once one discovers they are a great roofer, salesman, or programmer, they can get the double satisfaction of doing well and doing good. The fact that we all cannot be the CEO does not diminish the satisfaction of a man who does his job well, allowing those of various abilities to all reach some satisfaction. Further, the variety of skills needed in an economy imply that while 90% of people are bad at

any one thing, most people are good at

something. Mickey Kaus wrote a book in 1995 about the concept of

multiple social hierarchies, in that modernity allows us to find satisfaction somewhere via the law of comparative advantage; we like doing what we are good at, and via specialization, and the fact that good is relative, we can all find something that we like. It's not your aggregate popularity or wealth that matters, just that you have a circle of friends and acquaintances that provide you with what psychologist

Eric Berne called 'strokes' of affirmation obtained via parochial competence (like dogs we like daily petting). It's related to Arthur Brooks' concept of

earned success--the belief you are creating value with your life and in other people--as the basis for happiness. Interestingly, Brooks finds most happy people

anticipate more success in their job, and a whopping 95% of happy people are satisfied with their jobs. Micromanaging these jobs with more licensing restrictions, regulations, and taxes would not help these people.

Finding one's niche in life needs experimentation and creative license, and this needs low entry costs and autonomy. Government jobs emphasize credentials and make it very difficult to innovate, and government rules impose substantial barriers to entry via licensing restriction often made in collusion with industry groups (in everything from

health care to

hairstylists). Public teachers today have little ability to produce their own lesson plans, need specific degrees irrespective of their expertise, and are paid basically purely on seniority and whether they have a BA, MA, or PhD, surely a rule not good for students or teachers. Thus those whose job it is to study education and should know better, overweight credentials and experience for hiring and pay because that's what the democratically run system found fair. Decentralizing authority and letting principals hire and fire outside these criteria is anathema, an example of how democracy concentrates power in a

gosplan. In the Soviet Union many laborers, disillusioned by their lack of autonomy and the ubiquitous moral hypocrisy, would drink themselves to sleep every night, and so vodka and rum were subsidized in the Soviet Union and Cuba in recognition of the need for this kind of euthanasia; alienation in a state-run economy is much higher than in any private industry.

![]()

The government spends about 35% of GDP in the US today, and heavily regulates the rest. It would be far better if, instead of thinking about new tricky ways to squeeze the rich, we instead set government spending to some fraction (say 35%) of the past 5 years of GDP and no more. The endless arguments about the level would stop, and it's interesting to note that over the past 30 years in the US federal revenues as a percent of GDP has been remarkably consistent across various administrations. By using a moving average of historical GDP this would make spending countercyclical, most importantly instead of politicians being elected for their ability to promise 'more' they would instead focus on 'better.' That is, it would be nice if the politicians argued about better ways to allocate spending rather than about more or less in aggregate; the net result of the 'more' approach has been those who are good at articulating why we need more find they have no idea how to spend it, as when the government had $800B to spend in stimulus, most of it simply went to

shoring up state budgets, meaning, state pension deficits, which is just an income transfer to state employees from future taxpayers.

At one point Piketty notes rich countries are poor in that they are all deep in debt and have persistent deficit issues. Piketty insists government needs just a little bit more revenue. Given the historically high levels of absolute and relative spending by rich countries, it's highly likely that if we solved today's deficits with new forms of revenue, spending would rise and we would be back in the same position; governments seem destined to always spend a little more than their revenue.

Hegel argued that

Diogenesâ asceticism in the 4th century BC was a product of the luxury prevalent in the social life of Athens at this time, and Hegel himself saw a lot of existential crises in his times circa 1800 as people acquired desires for increasing the opinion of others. Now, those were times when wealth was much less than what Piketty considered 'abysmal' in the mid 19th century--how could they afford existential angst when they were basically literate cave men? Clearly a modest level of food and shelter, much lower than today's poverty line, is sufficient to unleash a man's search for meaning.

People like living together, as Socrates noted that a man that can live alone is either a beast or a god, and banishment from your tribe a fate worse than death. Affective neurologist

Jaak Panksepp has documented that seeking social interaction is as biochemically fundamental as the urge for sex and rage, making many mammals intrinsically sociable (or at least, if you've ever done cocaine--which hijacks these circuits--talkative). In addition to our sociability, we also seek status. As documented by anthropologist Dan Brown, status seeking is a

human universal, unlike greed, it affects serotonin levels and health outcomes, and fMRI studies show our concern for status is hard-wired. We can assume people want to interact and be esteemed by other people.

The anthropologist Harold Schneider studied hunter gatherers and noted they had an almost absence of hierarchy, which he saw as the resulting from the maxim that âall men seek to rule, but if they cannot, they seek to be equal.' It's a reasonable solution for a society without division of labor. Unfortunately many progressives see the world the same way, and thus like the Rawlsian solution that everyone has the same outcome regardless of one's talents or wealth. Now, that's fine for a camping trip, but in modern society unnecessarily.

Reality shows like

Top Chef, Project Ink, Project Runway, or

Deadliest Catch show people passionate about activities I do not care about in the least, all private sector jobs. With thousands of different remunerative specialties that complement each other, this allows us to focus and then trade with others to get the benefits of other's specialization focus. In modernity status isn't limited to one dimension, and so you can be an important part of something bigger than yourself without joining a religion: you are part of a complex network of specialists in a market economy of individuals maximizing their status in their own individual way.

Everyone wants to live on in the future in some way, as part of heaven or something worldly that needed or at least appreciated you. If you obey the laws and social norms, including The Golden Rule, and generate more revenue than you cost, you are making your tribe better off. The egalitarian solution where we have a single-payer state for everything has no risk, but like Hegel's farmer, promises little potential for self-actualization or what the Greeks called

arête ('excellence'), which in the modern world is consistent with specialization, trade, and productivity growth (

arête incents one to do things better than before).

We shouldn't base our norms on hunter gatherers, which is why most people don't.

![]() |

| Piketty Wants More Bubbles |

The idea that government spending increases welfare rests on the notion that spending "G" increases output however it occurs, in that G, I, and C all add to GNP. This is highly naive. Some jobs increase value by increasing the amount of goods and services ultimate consumed, and surely bridges and roads fill this function, yet many government jobs are little different than transfer payments because they do not add to the wisdom of any child, or increase the consumer or producer surplus of those in the market. This focus on aggregates and transfers therein encourages dependence on the state and discourages what the ancient Greeks thought were the only way to human flourishing, or

eudaimonia, was through virtue and character. Of course, theoretically more people are able to develop themselves via state welfare, but in practice the negative effects outweigh the positive. Indeed, people with neither the ability nor inclination to support themselves basically just create more such people, leading to a depressing end game (see

Parfit's repugnant conclusion, where a world of 1 billion human wretches is morally preferred to 50 million Aristotles)

Piketty doesn't spend much time on how the government might use the new revenue he thinks they should get from a new wealth tax, which is understandable because the main point is merely to have fewer rich people. Yet, it should give one pause that even cases where it seems easy to spend money well have not worked out well. For example, theoretically regulators will moderate financial crises, but in practice are inept at best. Consider the

CAMELS financial risk metric introduced by regulators in response to the crises of the 1970s and 80s was completely irrelevant to the latest financial crisis; if it were a business it would have died long ago, but it's not, so it just keeps wasting everyone's time. Progressives forget that regulators, academics, and legislators did not merely know about the relaxation of underwriting standards prior to the recent financial crisis, they

encouraged them to the point of mandating increased lending to lower-income demographics via reviews of potential mergers and direct legal action. Joseph P. Kennedy bought his way onto the first federal financial regulator job after becoming rich defrauding investors, and so unsurprisingly financial regulators have always been good at preventing competition under the pretext of helping widows and orphans.

A good amount of people are happy with jobs where their tasks are spelled out specifically and discourage innovation. Yet a lot of people find this stultifying, especially if they see the required duties as counterproductive. For example, many teachers are outraged by recent federally mandated

Common Core teaching curriculum for high school, because it is inflexible and bizarrely stupid. No wonder that the public sector and unions both have

higher rates of absenteeism than the private sector, because when your customers do not have a choice workers are paid but not esteemed, and that's important. At current levels of government we have more than enough jobs that do not require creativity. Not everyone can be a regulator, nor does everyone want to.

To those who merely care about equality, the details about how money is spent on health care or education, how a job is evaluated by those who create it, is of almost no concern, excepting when they occasionally reflect on the quality, which then immediately leads them to lobby for more aggregate spending. For example, progressive economist Lawrence Summers

laments New York's dilapidated airports as if the constraint is aggregate spending, but he's focused on the wrong bottleneck, in that case too many stakeholders with impossible demands. Equality and democratic process--i.e., Brahmins applying the latest intellectual wisdom to the masses as settled science--is all that matters, as if the economy is like a fighter jet and so needs a competent pilot. It is a hard thing for intellectuals to acknowledge the great benefits to society from undirected people who never so intended it, as even today the phrase 'invisible hand' is considered a concept on par with 'virgin birth.' It's an understandable instinct, as the majority of economists thought socialism was more productive than market-oriented economies back in the 1950s, because doing something for society seems obviously better than doing it for profit (eg,

Einstein thought it obvious).

Capital isn't a thing; it's a ledger, a way of determining who gets the make decisions about various things, and who gets the fruits of those things. The fact that a minority has most of the power to decide and access the fruits is a consequence of a past where individuals anticipated a future where such a ledger would continue to be valid. It's always been popular to think, maybe we should have a jubilee, get rid of those ledgers and start again as equals! Given the

power law distribution of wealth at all times such a proposal is perennially popular to those ignorant of history. Yet, if you do this every period, capital isn't owned by any individual, and so would be completely mismanaged as happens in societies without stable property rights. If you do this at all you can expect an immediately higher default premium which would make an economy undercapitalized. Luckily, our Founding Fathers specifically anticipated these problems and so emphasized the republican nature of our government, not making everything a democratic process.

The search for purpose often centers on one's job, and it's essential that most of these jobs have autonomy, which means outside of democratic control. A single-minded focus on equality and democracy misses that, leading to the terrifying future where the ideal is merely that everyone has the same amount of goods and privileges at all times, a world where I would need a lot of vodka and rum. Liberty, decentralized autonomy, and individual responsibility are considered pretexts for selfishness or bigotry, whereas libertarians see these ideas as pillars of a free and prosperous society; I'm sure this debate won't be solved in my lifetime.

![]() |

| Problem or Solution? |

A curative to this book is Peter Thiel's

From Zero to One coming out this fall. He's a billionaire, one of those whose very existence presents a problem to be solved for egalitarians. Thiel's book bristles with the enthusiasm of an entrepreneur, with tips on how to maximize your chances for success. At only 200 pages, it's a book meant to be read, not referenced. It's like positive psychology, focusing on habits of happy, prosperous people so one can become one. If you have a child graduating college, and he wants to be an intellectual, buy him Piketty's book; if he just wants to be a success in some vague unknowable way, buy him Thiel's.

.jpg "Facebook Twitter charts FB vs. TWTR")